When it comes to investing in the stock market, the choices are nearly endless. Growth, value, yield, ETFs … the list goes on and on. But one of the best combinations might be growth and income stocks.

Ideally, we can collect some income along the way, but also depend on the company to continue growing its sales and earnings, boosting its stock price. A company with a competent C-Suite can not only grow the business, but focus on returning capital to shareholders too.

That’s why we’re not looking for deep value names today or high-octane growth stocks. Instead, we’re focusing on a combination of growth and income stocks now and here’s a look at them. With the exception of one, we singled out stocks yielding 2% or more, sporting double-digit earnings growth this year and positive revenue growth this year and next year.

Compare Brokers

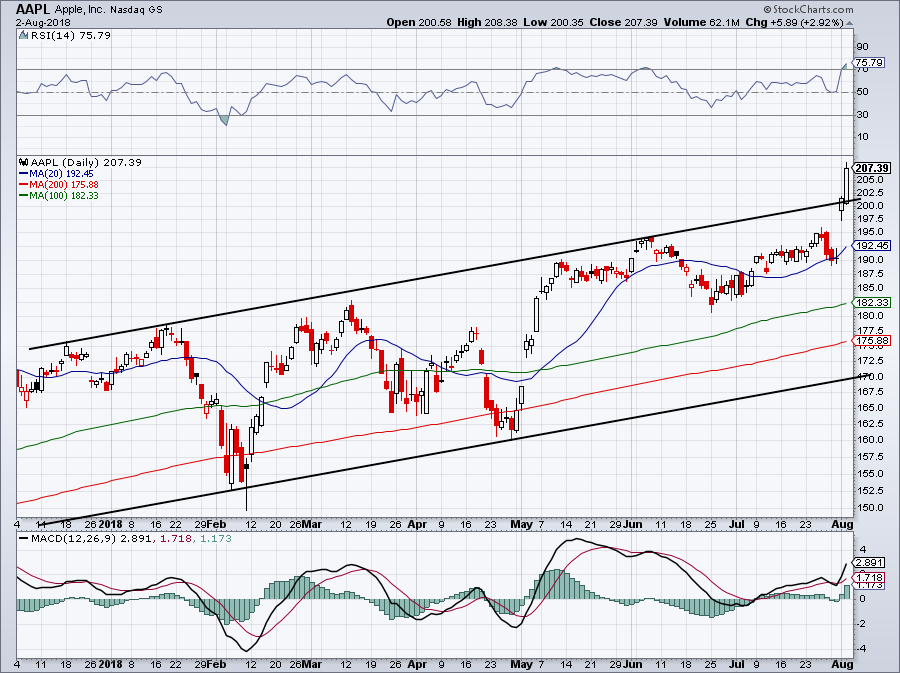

Top Growth and Income Stocks: Apple (AAPL)

After its latest earnings report, there was no way we could leave out the biggest of them all: Apple (NASDAQ:AAPL).

The tech behemoth reported a great result in what is its slowest quarter. Now heading into the second half and holiday seasons, how can we not like Apple? The company beat on earnings-per-share and revenue expectations, topped average selling price estimates for the iPhone and reported better-than-expected Services revenue.

Pretty darn good huh? Oh yeah, Apple provided better-than-expected revenue and gross margin guidance for the next quarter too.

With that in mind, analysts expect Apple to grow earnings 27% this year and 16% in 2019. On the revenue front, analysts expect sales to grow 15% this year and 5% in 2019.

It’s a little bit of a letdown for 2019, but the business is just too healthy to ignore. The profit machine that Apple has built around the iPhone, iPad, iPod and Mac is remarkable. But throw in the concept that all of these segments contribute to the massive, high-margin double-digit growth in its Services unit and not owning Apple seems crazy.

For reference, management expects this segment to churn out $50 billion in sales by 2020.

While Apple may only yield 1.6%, its buyback is another consideration. In May, the company announced a $100 billion share repurchase plan and ate up $25 billion worth of stock in the quarter. At this rate, I expect Apple to announce at least that much in its buyback next year too.

The dividend isn’t huge, but by allocating so much cash to the buyback and shrinking the float, it’s worth sacrificing some income. Especially when we can get it from the next four names.

Compare Brokers

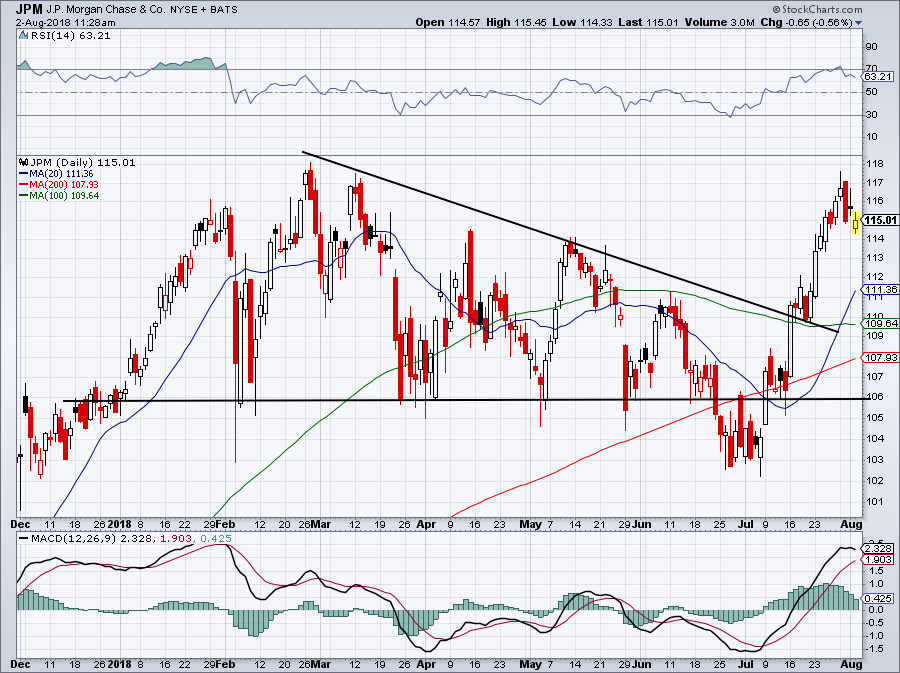

Top Growth and Income Stocks: JPMorgan (JPM)

Like Apple, JPMorgan Chase (NYSE:JPM) recently reported great earnings results. That’s not the only catalyst for JPM though, as the company passed the Fed’s stress tests with flying colors. It allows JPMorgan to buyback up $20.7 billion in stock over the next 12 months, while raising its quarterly dividend more than 40% to 80-cents-per-share.

That leaves the stock yielding about 2.8%, but that’s not the only good thing it has going for it.

As interest rates rise and the spread widens between short-term rates and long-term rates — in the short term anyway, because longer-term it’s still narrowing — JPMorgan and the rest of the banks become even more profitable.

Somehow, we’re getting JPM (and many of its peers) at a great valuation too. Shares trade at just 12.5 times this year’s earnings, which are set to grow more than 31% in 2018. Next year, estimates call for 8% growth, but that estimate continues to drift higher as we approach it. I wouldn’t be surprised by double-digit earnings growth in 2019.

On the sales front, analysts expect revenue growth of 7.5% in 2018 and 4% in 2019. At 12.5 times earnings, what more can you ask for?

Compare Brokers

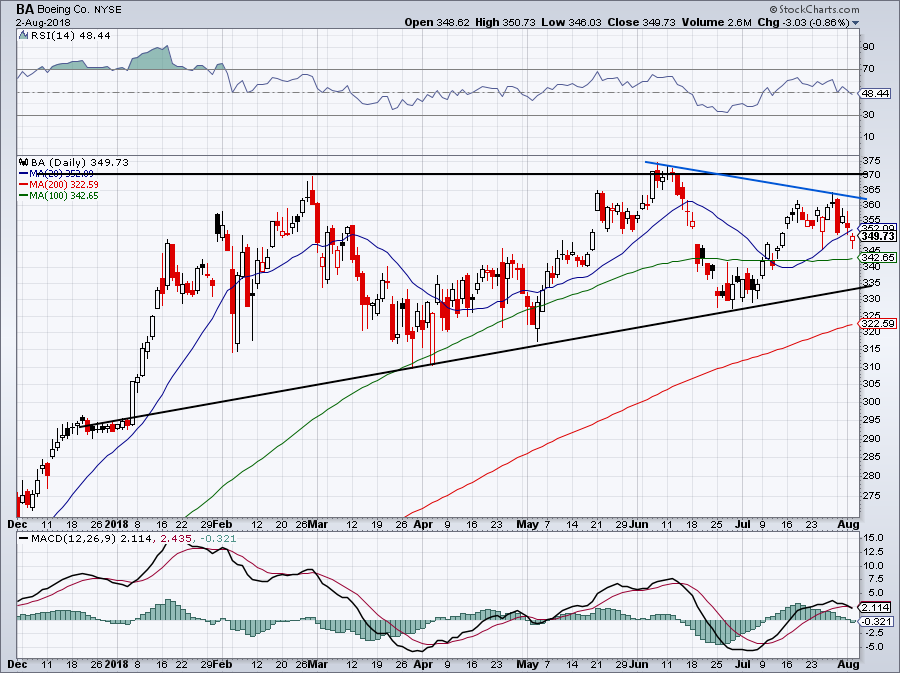

Top Growth and Income Stocks: Boeing (BA)

I was really going between Boeing (NYSE:BA) and PepsiCo (NYSE:PEP) for this spot. Not that you can really go wrong with either, but we ended up with Boeing.

Estimates call for earnings-per-share of $14.63 in 2018, up more than 40% from the prior year. Analysts expect another 20% growth in the following year, to go along with roughly 6% sales growth this year and next.

Boeing is a capital return story, plain and simple. While its revenue growth is solid and earnings growth is great, management continues to dump cash back to shareholders. In that sense, it’s a lot like Apple.

The company’s backlog consists of 5,900 aircraft worth almost $500 billion. Even with a recession — not that there’s one in sight — Boeing will have enough work to keep churning ahead. Its cash flows are as healthy as ever and this company is squeaky clean. Shares currently yield 2% to boot.

Compare Brokers

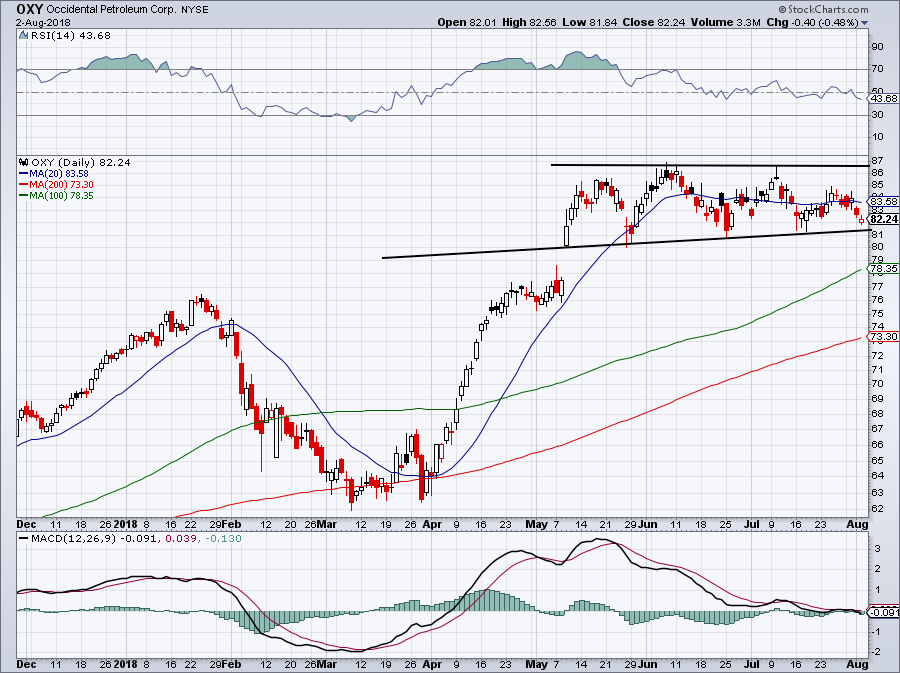

Top Growth and Income Stocks: Occidental Petroleum (OXY)

Not long ago we took a closer look at Occidental Petroleum (NYSE:OXY) and man were we impressed. Demand for oil continues to climb and so does its price. With disruption to foreign suppliers and more demand for domestic oil, OXY and its U.S. counterparts are natural winners.

After earning less than $1-per-share in 2017, OXY is on track to earn almost $5-per-share this year. That leaves the stock trading at just 16 times earnings. In 2019, that figure is expected to grow 7% to about $5.25-per-share. However, like JPM, that figure could prove conservative as estimates continue to creep higher.

On the revenue front, analysts expect sales to grow about 30% this year and another 9% next year. Also like JPMorgan, having a strong economy at its back should help the oil market and thus, help Occidental Petroleum.

On the dividend front, management just gave a slight increase to its quarterly payout, up a penny to 78-cents-a-share. That’s good for a whopping 3.8% yield.

Compare Brokers

Top Growth and Income Stocks: Starbucks (SBUX)

Saving the most controversial of them all for last, we have Starbucks (NASDAQ:SBUX).

Starbucks was once the do-no-wrong, fast-casual turned tech company that Wall Street absolutely adored. It took some convincing, but once investors saw the kind of spunk Starbucks’ app would provide its same-store sales and revenue, shares soared. That is, until about 2016. Going on 30 months now, Starbucks has been trapped between the low $50s and $60, with shares now hovering on the lower end of that range. To say it has been disappointing would be an understatement.

Last quarter we saw bad numbers out of China and underwhelming same-store sales out of its main market in the U.S. But curiously, shares rallied on the report. Could this be a sign that the bad news is fully priced in?

After all, Starbucks is still a profitable company and is still churning out record results each quarter. While there’s been a hiccup in China, the immense growth story still seems on track. It’s not like Starbucks is broken, it simply just isn’t growing like it used to and is getting a lower valuation as a result.

There’s really nothing wrong with that.

The company is closing underperforming stores, shifted out of its consumer-packaged goods operation in a $7.2 billion alliance with Nestle and is focused on improving its operational efficiency. Trust me, there are worse things investors can hear from management.

Estimates call for 17% growth this year and 10% next year, along with 11% sales growth this year and 7% in 2019. After its deal with Nestle, SBUX announced a 20% increase to its dividend, following a 20% increase in November. Shares now yield 2.8%, while SBUX bumped its total capital return to shareholders from $15 billion to $25 billion through fiscal 2020.

Keep in mind, SBUX has a market cap of “just” $71 billion, so these returns are no small sum.

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell. As of this writing, he was long SBUX, A